Trending publication

Bonus Depreciation Regulations: A Guide to Tax-Free Income from Capital

Print PDFEconomists maintain that income generated from an expensed capital asset is tax-free. We can’t verify that claim. We can confirm that expensing capital assets enhances investment returns. For this reason, bonus depreciation matters to your capital investment decisions.

The Treasury Department issued final and proposed bonus depreciation regulations on September 6, 2019 (the “2019 Regulations”). These regulations guide us in planning to maximize returns on capital investments. This advisory highlights the key points of those regulations. In future advisories, we will cover these points and others in depth.

Bonus depreciation applies to tangible property with a 20-year or less recovery period. Most machinery and equipment is recovered in less than 20 years. Real estate is not, except for land improvements recovered over 20 years. Unfortunately, Congress inadvertently omitted qualified improvement property (e.g., tenant improvements) from 15-year property in the enacted statute. As a consequence, qualified improvement property will not qualify for bonus depreciation. Internal Revenue Service correctly declined to fix the error.

Bonus depreciation applies to original use property. Original use means the first use to which the property is put, whether it’s your use or someone else’s use. Also, the first use remains the original use even if the property is repurposed. However, if the property is reconditioned or rebuilt, that property can be repurposed, and that repurposed use can be the original use.

Bonus depreciation can apply to some used property, too. The property must be “purchased” from an unrelated person in a taxable transaction. Further, neither the purchaser nor its predecessor can have had a depreciable interest in the property during a 5-year look-back. The defined key terms used in these tests – “purchase”; “unrelated”; “predecessor”; “depreciable interest” – define the scope of used property eligible for bonus depreciation.

Bonus depreciation can apply in a 336(e) transaction. Some stock sales may be treated for tax purposes as asset sales under Sections 338 and 336(e). Section 338 applies where one corporation acquires stock of another corporation. Section 336(e) can apply where the acquiror is not a corporation. In each case, assets acquired are depreciable. However, for purely technical reasons, only assets acquired in Section 338 transactions qualified for bonus depreciation. The 2019 Regulations changed that. Now, assets acquired in a Section 336(e) may also qualify for bonus depreciation.

Special rules apply to partnership transactions. Partnership interest transfers and liquidations can trigger positive basis adjustments in partnership assets. Some of these basis adjustments can be recovered with depreciation deductions. Bonus depreciation can apply if the basis adjustment results from a sale of a partnership interest and it is not attributable to contributed built-in gain property. Bonus depreciation will not apply to basis adjustments resulting from interest redemptions/liquidations.

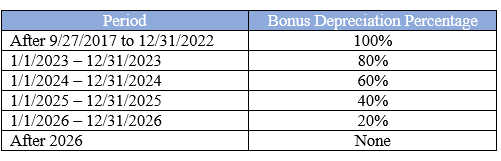

Bonus depreciation phases out. As you can see in the table below, eligible property acquired and placed in service after September 27, 2017 but before January 1, 2023 qualifies for 100% bonus depreciation. Eligible property placed in service after 2022 qualifies for a lesser amount.

This advisory was prepared by Nutter's Tax Department. For more information, please contact your Nutter attorney at 617.439.2000.

This advisory is for information purposes only and should not be construed as legal advice on any specific facts or circumstances. Under the rules of the Supreme Judicial Court of Massachusetts, this material may be considered as advertising.